Bitcoin In 1 Hour

Introduction

Hi, I'm Jeremy and I absolutely love Bitcoin. In 2013, a friend mentioned the word Bitcoin to me and I have been obsessed with it ever since.

At the time, talking about Bitcoin was seen as fringe and possibly a little crazy. But as time has passed, Bitcoin has proven to the world that it is a robust and valuable innovation. It has pioneered the cryptocurrency industry, which has grown from nothing to more than a trillion dollars in about 12 years, roughly half the time it took Google to reach the same size. It has legions of avid supporters and just as many vocal critics. It has inspired documentaries, books, artwork, music and everything else imaginable.

However, despite its prominence, Bitcoin is still very commonly misunderstood. People are bewildered by a constant stream of hyperbolic headlines, scams, misinformation, price volatility, new cryptocurrencies, mixed messages from companies, governments or banks and much more besides. It's hard to make heads or tails of what any of this is about, yet it seems like the world is rushing towards it at an incredible pace.

That's what I'm here to fix. To solve this problem I created this article series - Bitcoin In 1 Hour. It's a series of 10 short episodes, 5 minutes each, so that in under 1 hour you can properly understand what Bitcoin and cryptocurrency is all about. There is no prior knowledge required, and I promise that if you read it from start to finish you will feel much more confident in your own research or the next time cryptocurrency is mentioned at an office party. It's broken up into chunks so you can take it step-by-step or plow through it all at once, and it should be easy to revisit each piece as many times as you need to. There is a lot to think about, and while cryptocurrency moves fast the fundamental ideas in this series do not go out of date so don't rush and take it at your own pace.

Here is the breakdown of the episodes:

- Money

- Bitcoin

- Philosophy

- Blockchains

- Government

- Banks

- Adoption, mania and scams

- Bitcoin Cash

- Ethereum, Dogecoin, Tether and more

- The future

If you prefer an audio format, most of the same ideas are explained in Episode 85, which is the best episode of the Podcast to start with.

We'll start by talking about the history of money, how Bitcoin fits into the story, how it works and why it came about. Next is how cryptocurrency has grown, how this has been handled by government and banks, and the general market mania around cryptocurrency. Then we'll look at how cryptocurrency has grown beyond Bitcoin with Bitcoin Cash, Ethereum, Dogecoin and other types of coins. And finally, we'll talk about the future and why cryptocurrency is set to change the way people organise themselves in society. That's a lot to cover, but I promise we can fit it into just one hour.

Before we get started, one quick disclaimer.

I am not a professional financial advisor, this is not investment advice blah blah blah. Don't worry, I'm not here to tell you about getting rich. What I will do is my absolute best to demistify all of the volatility and speculation that goes on in cryptocurrency, so you can see the forest for the trees. In cryptocurrency, people often say "Don't invest more than you can afford to lose", but I prefer to say "Don't invest more than you can understand." Everybody's financial situation is different, but if you know what cryptocurrency is about and how it works, you will be able to make the best decisions for yourself - whether that is completely avoiding cryptocurrency or changing your entire career to join the industry or anything in between, the best choice is different for everyone.

Alright, that's it, I hope you enjoy this series, welcome to Bitcoin in 1 Hour and I'm glad you're along for the ride. I'll see you in Episode 1 to talk about the thing that makes the world go round: MONEY.

Episode 1 of 10: Money

They say it makes the world go round, doesn't grow on trees and it can't buy happiness. Wars have been fought over it, business empires built, lives wasted and nations destroyed. Some people are good with it, and some never have enough. Almost everyone uses money every single day, and yet its existence is generally taken entirely for granted. Education about our financial system is suspiciously absent from schools, universities, the media and even places you think it would be well understood such as banks or Economics think tanks. If nothing else, public consternation over Bitcoin is undeniable proof that the world is not much used to thinking about money, and that collectively we have a lot of hidden assumptions about money that are surprising or confronting when brought to the surface.

Is this money? Do you trade physical cash like this more or less often than numbers on a screen via mobile phones, credit cards or online banking? Why do videogames often represent money as weights of gold instead of paper?

When you think of money, you probably think of something like this, a physical paper or polymer note issued by your local government and maybe metallic coins for small denominations. You know you can work for more of it, and trade it with other people for things you need. But if pressed, it might be hard to provide a rational reason for why pieces of paper are worth trading valuable time and skilled labour for except that everyone else is doing it or that's just the way it's always been.

Of course, that's not the way it's always been. Throughout human history, people have used all kinds of things to trade as money. Seashells, beads, salt, gold and silver, sheep and cattle, poker chips, trading cards, even large unmovable rocks. Famously cigarettes have been used as money in prisons or during war time, and video games or science fiction movies may have a variety of commodities or credit systems in use. You may operate an informal bar tab arrangement with your friends or family that is rarely if ever settled in cash, or unquestioningly accept an entirely different system of money when playing a game of Monopoly or travelling to another country.

It's very apparent that, given the right circumstances or environment, anything can be traded for anything. But a freeform system of barter is heavily impractical, as matching goods in exactly tradeable quantities is difficult to do without a common reference point. Therefore any human collective will naturally and rapidly adopt a central good as its most tradeable commodity to facilitate commerce. The choice of goods is not random though, and highly prioritises items with the best mix of the following 6 attributes:

-

Scarcity: Money needs to be limited in supply. The reason we don't use blades of grass as money is that if anyone can have as much money as they want, then it is fundamentally worthless. If the government gave every single person 100 trillion dollars tomorrow, that wouldn't make everyone rich or increase the amount of goods available to buy - it would just make money worth a lot less. This is exactly what happens in hyperinflation scenarios like Weimar Germany or Zimbabwe, and the out of control money printing ruins the economy instead of bringing prosperity. The exact quantity of the limited amount of money is not important, just the general premise that there is a limit on supply, and therefore can be trusted to retain value.

-

Portability: Money has to be easy to transport, in small or large quantities. Concrete bricks are a terrible kind of money because it's hard to carry to the store to buy your coffee. Hence the popularity of very portable paper notes, bank cards, and their extension over the internet via online banking.

-

Durability: Money needs to last throughout time. We can't use bananas as money, because the banana you have today will be going bad in just a couple of days, and rot away completely within a few weeks let alone a year. Obviously it won't preserve your purchasing power very well for longer than a day or so. Money also needs to easily survive wear and tear, because it is always being handed around. This is why metal coins are often used and not glass or plastic, they hold up better to the rigours of being passed around, dropped, clattered together or rained on. Electronic money is even better, since as long as the servers stay online it never degrades.

-

Divisibility: Money has to support easy subdivision and combination. A system of barter is not sustainable because it is hard to trade two and a half chickens for three quarters of a pig. If money is going to be used to facilitate trade, it has to be easy to divide into smaller quantities and just as easy to recombine into larger amounts as transactions demand. Hence different denominations of paper notes/coins, or the inbuilt precision of electronic payments.

-

Fungibility: Related to divisibility, money needs to be uniform and regular. Watercolour paintings are terrible things to use as money, because one Van Gogh painting is completely different from a Picasso painting, or even from another Van Gogh painting. In contrast, one bar of gold is much the same as any other bar of gold that weighs the same, or one $5 note pretty much equivalent to any other $5 note - other people will not quibble about receiving one specific note in commerce, a $5 note is a $5 note.

-

Recognisability: Related to scarcity, money has to be easy to identify. If someone can make a fake dollar bill on their home printer and spend it at the store without being detected, before too long they will have printed themselves enough money to buy whatever they want and simultaneously made everyone else's money worth a lot less. Therefore money needs to be easily verifiable by each individual as they are trading for it, to avoid the proliferation of counterfeiting scams that debase money supply and unfairly reward counterfeiters.

Consider some of examples of money mentioned previously (e.g. seashells, salt, gold, poker chips, Monopoly money, government currencies) and how they match up to those attributes. Then head along to the next episode, where we get to the main attraction: Bitcoin.

Episode 2 of 10: Bitcoin

Ok, now we know what characteristics define a good item for money, we can turn to the main game: Bitcoin.

For many years, cryptography experts and free market thinkers have pondered the possibility of making a form of electronic money. By default, electronic money would be very portable, divisible, fungible, recognisable and durable - since it would consist only of electronic signals over the internet. However, the stumbling block was the first and most important aspect of money - scarcity. Making a digital money was not possible, because anyone who had a small amount of it could copy-and-paste it a billion times to make themselves an unlimited supply, and since anyone could do that it would soon become worthless.

The obvious solution is to have someone in charge of verifying the supply - such as a government, bank or company. This is how your online banking works. The problem with that is it gives the bank control of the system, and they can increase or decrease the supply, reverse transactions, block transactions they disagree with politically or delete your money at their own discretion. These bank systems have been workable to some extent, but in a politically divided world it's impossible for everyone to universally adopt a co-ordinated payments system as long as one central party with their own agenda has full control.

This is where the story of cryptocurrency begins. Until Bitcoin, it was not known how to have a digital item that was limited in supply, unless it was monitored and verified by a single party.

This changed in 2008, when the anonymous creator Satoshi Nakamoto published the Bitcoin whitepaper online. His paper, titled "Bitcoin: A peer-to-peer electronic cash system" detailed the technical specification for an online currency where no central party (no individual, bank, government or corporation) was in control. None of the people involved need to trust each other or even to know who they were dealing with. No-one in the system is able to cheat, print themselves free Bitcoin or stop anyone else transferring their Bitcoin for any reason.

This is the real reason Bitcoin is important. It is the invention of digital scarcity, the first kind of electronic or Internet object which could not be copy-pasted to make more of it, and even better it came with the inbuilt ability to be transferred in any quantity to anywhere (almost) for free.

Satoshi's solution to having one party control the circulating supply and history of transactions like a bank does, was to give EVERYONE the history of transactions. In a group of 100 people, 99 of them would naturally prefer to ignore any single individual claiming they had more than their allocated share of Bitcoin, and therefore the system is secure so long as the majority of participants remain honestly committed to the idea. To prove that the ledger maintainers were serious about their investment in the system, they were required to put their own money on the line in a way that could not be faked - by paying for electricity. Since humanity only has a limited supply of energy, and getting it is costly, cryptographically proven expenditure of energy is as close as humanity has to a universal resource. This process of network participants demonstrating their sincerity through unfakeable signals (expended energy) is called Bitcoin mining.

Participants in the system are able to add to the global history of transactions, called a blockchain, by using "wallet" software to add transactions that send Bitcoin from their address (similar to a reusable email address) to someone else's Bitcoin address.

Think of the Bitcoin blockchain as a public Excel spreadsheet, where individuals have their balances noted as they would in a bank account. Old system: the bank has a single private spreadsheet, and they control the money. New system: Everyone in the world has a public spreadsheet, and no one controls the money. Everybody is confident in the veracity of this new Bitcoin ledger because it is publicly auditable and it is "backed" by a huge network of self-interested and specialised Bitcoin miners that are not owned by any single party.

Thus a new form of money was born. An electronic cash payments system which was better than government currencies because it was politically netural and limited in supply (could not be printed at will), and better than precious metals like gold because any amount of it could be sent anywhere in the world instantly for less than 1 cent.

A slightly cheaper and faster transaction system sounds cool and maybe useful, but it doesn't explain Bitcoin's legions of fanatical fans. To understand why Bitcoin has attracted so much attention for what seems like a more complicated PayPal, we need to momentarily set aside economics and take a detour into the abstract realm of philosophy. More on that in the next section.

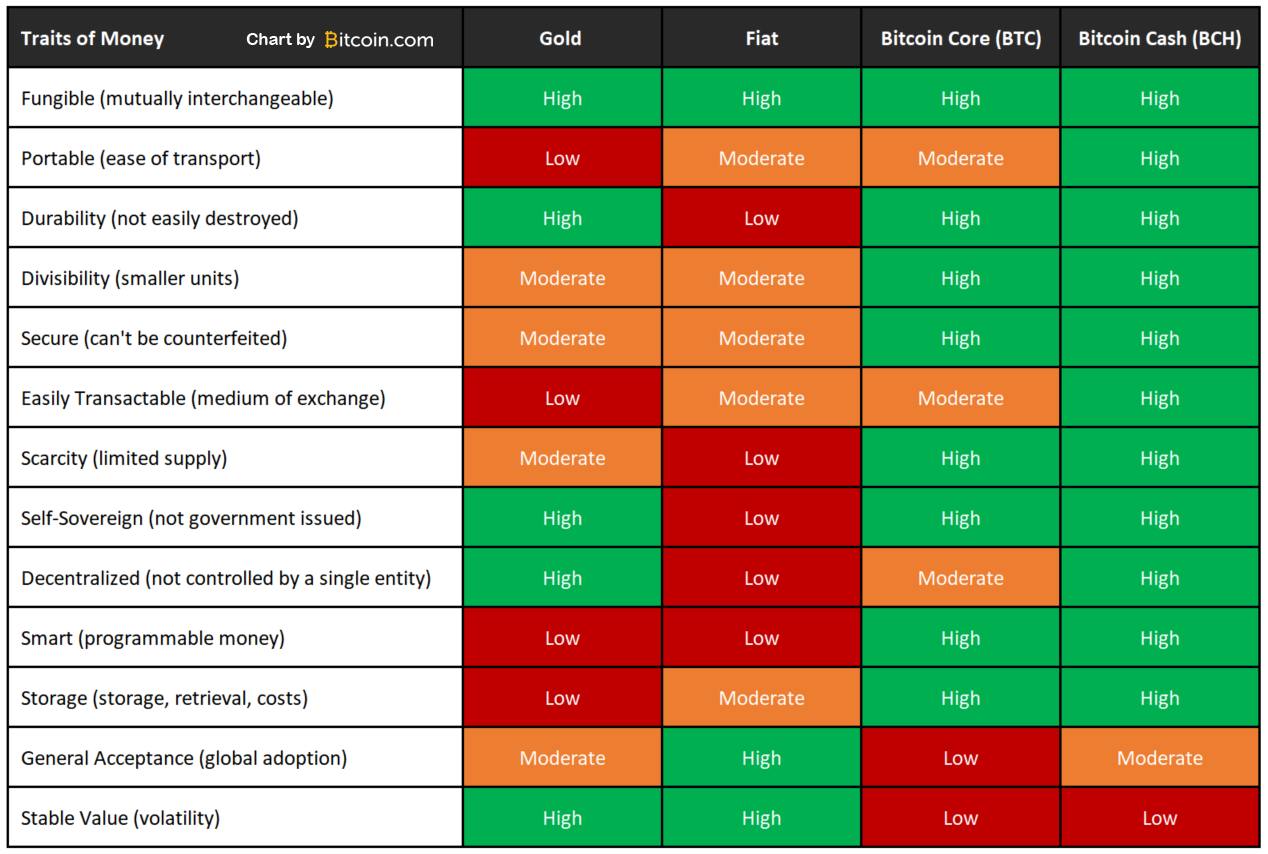

Before moving on, take a moment to compare the attributes of money. The difference between Bitcoin Core (BTC) and Bitcoin Cash (BCH) will be explained in Episode 8

Episode 3 of 10: Philosophy

In and of itself, Bitcoin has no political ideology - in the same way the wheel, the internet or the tennis shoe have no agenda, they are simply useful pieces of technology available to anyone who needs them. That said, Bitcoin's founder Satoshi Nakamoto and its early community advocated a very specific set of principles and beliefs, which contributed heavily to its success and remain essential to understanding cryptocurrency to this day.

This community was known as the "cypherpunks" (cypher, like a cryptographic code, not "cyber" punks). They believed that human rights such as privacy, freedom of speech and freedom of trade could be guaranteed with cryptography - as mathematics is netural, objective and incorruptible in a way that human dispute resolution systems like courts can never match. It is impossible to shoot or violently coerce someone over an anonymous Internet connection, and therefore it was considered plausible to make a system of violence-free commerce which allowed parties to transact anonymously and without central oversight. For many years, the cypherpunks struggled with finding an implementation of digital money based on cryptographic proofs instead of government approval, and Satoshi's publication of the Bitcoin whitepaper was the first working solution.

In a word, this cypherpunk philosophy is probably best described as "crypto-anarchy" but many early Bitcoiners will variously describe themselves as voluntaryists, anarcho-capitalists or libertarians. The foundational principles of these schools of thought include:

- Obsolescence of Trust: Often said as "Verify, don't trust", Bitcoiners prefer to create systems where mathematical certainty can underlie a system instead of the perpetually unreliable promise of an individual or group.

- Free-market commerce: Cryptocurrency is built on the idea of voluntary exchange creating prosperity for both parties, since if it didn't they wouldn't agree to trade! In other words, a very pure, unregulated, form of free-market capitalism. Therefore crypto communities are largely against the interference of government authorities, who are often seen as a hinderance. Government ultimately imposes its will via violent military force. In contrast, cryptocurrencies stand against violent coercion, encouraging voluntary exchange.

- Freedom from central interference: Cryptocurrency communities generally contain a high level of suspicion of government. One of the earliest use cases for cryptocurrency was to send money to WikiLeaks journalist Julian Assange, after his other donations methods were shut down by the government. Crypto communities also usually view with suspicion any kind of collectivist activity, preferring to bet on the "invisible hand of the market" to guide individuals to optimal decision making. This does not mean charity or co-operation is frowned upon, actually those are both very prevalent in the cryptocurrency community, but it does mean they only operate entirely voluntarily and sometimes anonymously (without external validation-seeking).

- Censorship resistance: Just as Bitcoiners believe in a free market of trade, so too they believe in a free market of ideas. For a free market of ideas, it is critical that individuals cannot be "deplatformed" for holding contrarian or fringe views. This is particularly pertinent as Bitcoin itself started as just such a fringe movement. Supression of free speech at the extreme leads to a dystopia of the kind famously enunciated in George Orwell's book 1984, and even the harshest words cannot cause physical harm, maintaining consistency with the focus on peace and lack of violence.

- Peaceful co-operation: Combined with strong anonymity across a non-physical medium (i.e. internet communication), violent coercion is not merely impractical but literally impossible. This guarantees any trade must occur in a free market, the protection of individual rights. It also naturally explains the distrust of government, who fundamentally rely on the threat of force (via a military or police force) to collect taxation or enforce any other rules or regulations.

- Privacy: Satoshi Nakamoto maintained total anonymity until his disappearance in 2011, and not without good reason. Founders of other non-governmental monetary systems in the 1990s and 2000s such as e-gold and Liberty Reserve found themselves regularly afoul of the law and prosecuted or jailed simply for offering alternatives to government fiat currencies. In this tradition, many cryptocurrency communities contain prominent members that are only known pseudonymously. Thus their ideas or contributions are judged solely by their merits as ideas rather than by reference to the personal characteristics of their source. This simultaneously protects those individuals from government or adversarial interference.

These ideals are important to understanding Bitcoin and cryptocurrency not merely as an economic advancement, but as a humanitarian social revolution creating a more free, peaceful, voluntary society. The ideological and economic aspects of Bitcoin form a virtuous cycle - Bitcoin succeeds by adhereing to its founding princples, and by succeeding it draws increased freedom and economic resources to those who support it most passionately, giving them increased capability to continue moving the movement forward. This very Bitcoin tutorial is an example of this process - the funds to produce it were earnt directly from the cryptocurrency community.

It is essential to understand that critics do not need to agree with the Bitcoin community's philosophy to find the financial network itself economically useful and thus spread its influence. The Bitcoin community also welcomes any competition against this economically-embodied philosophy, hence the proliferation of thousands of alternatives cryptocurrencies. If critics have the idea and passion for a better economic, political or philosophical system then all they have to do is prove it! Critics are even given a head start because all the software for Bitcoin is freely available online, and they are free to modify it in whichever way they like (for example, individuals that dislike capitalism and believe in mandatory wealth redistribution or a different method of supply issuance can create and advocate that kind of cryptocurrency). The hard part of competing is not creating a copy of Bitcoin, the hard part is convincing people to use it! Any competitor would need to demonstrate its superiority by logically and peacefully convincing more people to hold and transact with that coin than hold and transact with Bitcoin itself. This challenge is not easy, particularly since the neturality of a currency is hard to establish when it has only just been founded or has a small number of users.

So far, no other coin community has successfully taken the #1 crypto position from Bitcoin, but not for lack of trying and not without significant progress towards success. Bitcoin's market share has declined from its original 100% to around 40% of the cryptocurrency market (its closest competitor, Ethereum, has risen to around 20% share). We will return to those competitors in Episode 8 and Episode 9, but for now let's take a look at the technology that enables it by discussing the mechanics of a Blockchain.

Episode 4 of 10: Blockchains

Ok so now you know what Bitcoin is and what it represents. Let's turn our attention to how it works, by discussing the actual mechanisms of a blockchain. You don't need to understand every single detail and I won't go into all of the technicalities here, but a high-level understanding of how Bitcoin is put together can help it make a lot more sense. This knowledge will be particularly useful when evaluating other cryptocurrencies, which are discussed in Episode 8 and Episode 9.

Before starting, it is important to note that blockchains have received a lot of hype for use in all kinds of industries. They may indeed prove useful in ways that no-one yet expects, but it is also true that a vast majority of projects will fail - much like how many websites went bust in the dotcom boom of the 1990s to discover which ones were the valuable websites and Internet we enjoy today. In many instances, a central database, such as every existing technology company is already using, can do the same data storage job as a blockchain but better. Blockchains are NOT a total replacement for every technology product in the world, but in some cases, such as use as a currency, the tradeoffs they make can be incredibly valuable.

Fundamentally, a blockchain is simply a public list of transactions, like an Excel spreadsheet publically accessible online. The transactions are stored on a public network of computers (called "nodes") around the world, which anyone can join at any time. The nodes scan transactions to make sure they follow the rules of the network, and announce transactions they hear about to other nodes so that all new information spreads to all nodes. The transactions are collated together into blocks of transactions, and each block links to the block before it - which provides the chronology of transactions and gives rise to the name "blockchain".

Any individual can announce a new transaction by telling a node about it. This is what happens when one person sends Bitcoin to another person, they are simply announcing "I have these 4 Bitcoins, and I would like to make a transfer of 2 of those Bitcoins to this new address." That message is then relayed around the entire network and is picked up by the recipient, similar to the way sending a text message or email works.

Any node can announce a new block of transactions, and in return receive the transaction fees from the transactions as well as some newly minted coins. To ensure block announcements are spread out among nodes and to guarantee nodes cannot cheat and announce invalid blocks, each new block is only valid when it includes a secret number called the "nonce". The only way to find the nonce is to guess over and over again, so it is like a random lottery ticket only valid for announcing that block. Bitcoin mining is simply the process of nodes expending computer energy guessing over and over again for this "lottery ticket" to announce the next block (and receive the new coins and transaction fees for doing so). Contrary to the common misconception, Bitcoin or other cryptocurrency mining is not "wasted" energy, it is the energy spent to secure the network similar to the same way a bank's computers secure its transaction records. The amount of energy spent is equal to the value of the new coins, so cryptocurrencies only expend energy because people find a free economic system valuable and are using it in transactions. The difficulty of the network automatically adjusts up or down to compensate for miners joining or leaving the network, so that while each block is generated at random, over long periods of time the rate of new coin issuance is predictable. In the case of Bitcoin, the network targets a new block every 10 minutes, but other currencies use other intervals.

The "password" needed to make a transfer of Bitcoin is called a "private key" (often represented as a "seed phrase" of 12 words which makes it easier to backup). As an individual cryptocurrency holder, it is critically important to backup this seed phrase (as it can recover the coins in the case of a lost or broken device), and just as important to keep it a secret because anyone who knows the seed can take all of your coins!

None of the cryptography needed to run Bitcoin is incredibly new. The genius was in the combination of existing elements to bind them together to form economic incentives for people to invest in the system without needing oversight and with penalties for cheating.

One other important note about blockchains. A blockchain cannot guarantee the integrity of any physical assets in relation to itself. This is a common oversight that proponents of gold-backed cryptocurrencies or fiat-pegged cryptocurrencies often miss - the genius of a blockchain is not that its tokens can be redeemed for something, it's the opposite - there is nothing to redeem! The tokens themselves are verified and guaranteed by the network, and cannot be faked. Provided they are limited in supply and have consumer demand - that makes them a potential form of currency. Adding external assets creates unnecessary counterparty risk - i.e. the person who holds the gold or currencies may refuse or be unable to pay up in exchange for a cryptocurrency token. Why bother with a token verifying network, if you want to trade something that ISN'T those tokens?

Ok time to turn to governments, and how they have responded to this new ungoverned, cooperative social and economic movement.

Episode 5 of 10: Government

Governments are the only institutions in society which independently produce nothing of value. All they can do is redistribute wealth from one place to another - to public goods or to politician's pockets - and often very inefficiently at that. They are able to get away with this because they generally have a monopoly on the legal use of force, that is they are the ones in society with the most guns. Remember in Episode 3 that the "cypherpunks" were opposed to this societal organisation by violence. Despite its lack of productivity and immoral enforcement methods, the government still has endless appetite to expand its own power and spending. To fundraise for these redistribution efforts, it taxes the population in 1 of 2 ways.

The first and most obvious is income tax - the familiar slice of an individual's paycheck which goes to paying off the government every year. This method has its limits however, as the pain of raising the income tax is directly felt by citizens. At a certain point on the way to 100% income tax, increasing income tax becomes unsustainable, political pressure to reform hits critical mass and/or a revolution starts.

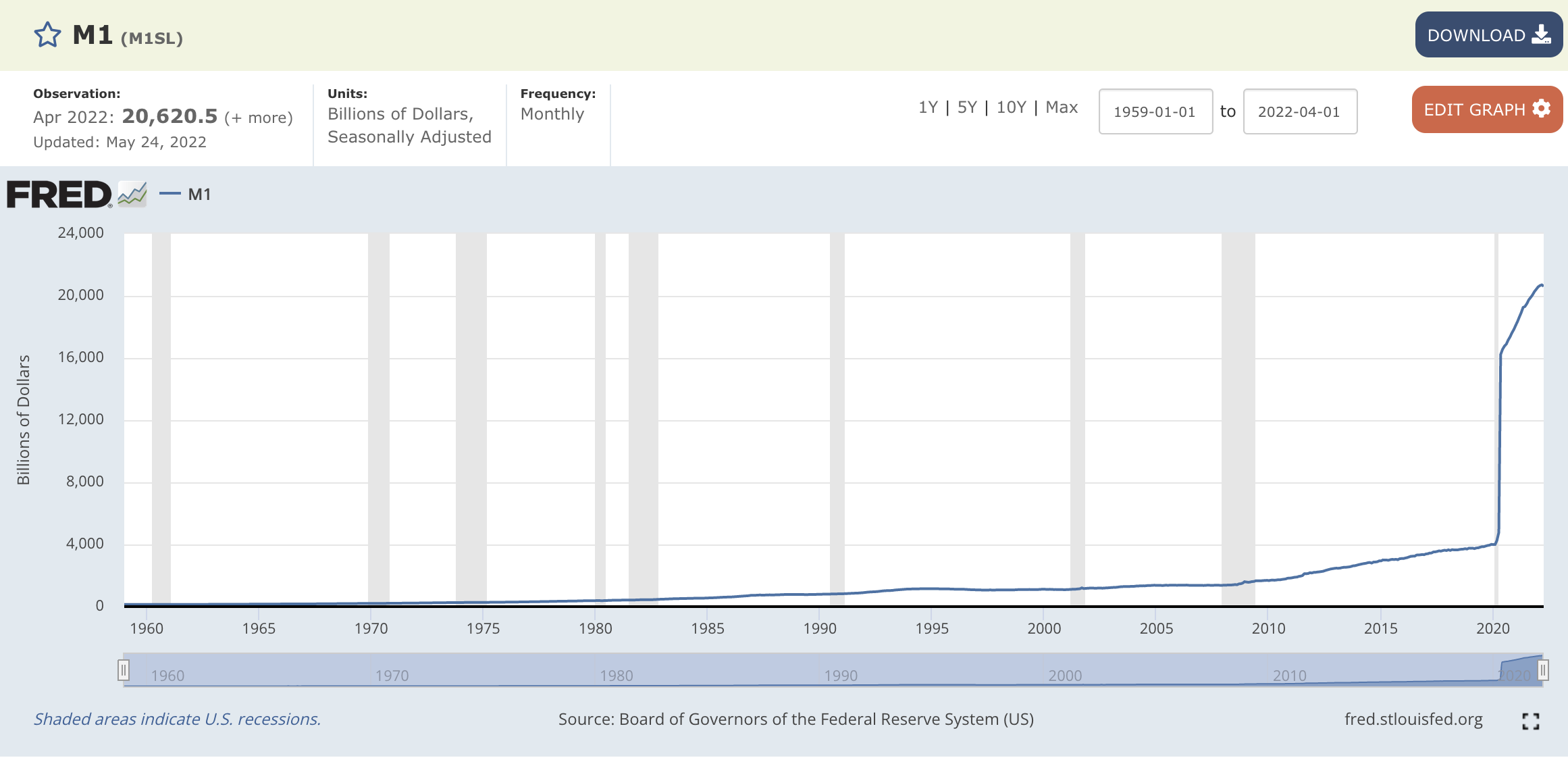

To get around this, the government turns to its second and much sneakier form of taxation - creating new fiat currency. If the government prints a new dollar for every dollar already existing they have not increased the amount of real wealth (goods and services) available in society, merely halved the value of the existing dollars. Remember from Episode 1 that every dollar is interchangeable, which is the "fungibility" property of money. The spending power is leeched from the existing dollars held by the population and transferred into fresh dollars owned by the government. Those dollars get spent, and the cycle repeats. This is the cause of inflation, the constant creation of new dollars leads to rising prices as more dollars chase the same amount of stuff. To protect their wealth from constant debasement, citizens move their savings into assets which cannot be constantly devalued - real estate, stocks, precious metals and now Bitcoin. We are now entering one of the highest periods of global government inflation in history - more than 30% of all the US dollars in the world were created in 2020. Therefore, the #1 biggest driver of cryptocurrency adoption is actually the government themselves! The more they print, the faster people wake up to the need to preserve their savings with a limited supply currency.

US Dollar M1 Money supply to Apr 2022. Yes, that's not a healthy looking chart. If you're noticing rising prices in your area, this is why. If you don't live in the US, the same thing is almost certainly happening to you and for the same reasons, all governments operate identically in this regard. Source: St Louis Fed

This incredible power of inflation is so important to the government that they go to great lengths to shut down any attempt to create an alternative form of money. An example of this was called "Liberty Reserve", which operated a private gold-backed currency in the early 2000s until they were shut down by the US government. This time though, the government doesn't have that option. Bitcoin has no central issuer, no central server to shut off, no CEO to arrest and no headquarters to raid. The network is globally distributed so that no individual government or even a coalition can effectively switch off or destroy it. The utility of politically netural and debasement free money is so high that the cryptocurrency community can profitably run and maintain the infrastructure in a decentralised manner that thwarts any direct attack from government. In this way, the government is rapidly losing control of their ability to control the supply of money - and they are losing it to the globally rising cryptocurrency social movement, who are voluntarily defecting one-by-one from government-based money.

The government's capacity to stop cryptocurrency is hampered by more than just the geographic distribution of the network. We are conditioned to thinking of governments as monolithic, semi-omnipotent institutions. This is largely untrue. A government is merely composed of a collection of individuals, who operate according to their own selfish interests (as can be seen by constant political scandals everywhere in the world), wrapped in the veneer of a larger framework. Because of this, cryptocurrency is perfectly designed to infiltrate and subvert governments. Individual public servants can understand cryptocurrency's superior monetary properties and invest in cryptocurrency just like any other member of the public. Once invested, they become a silent advocate of cryptocurrency, quietly acting in the interests of cryptocurrency adoption to benefit their own investments.

As the old saying goes, if you can't beat them - join them. Just as any rivals to Bitcoin are welcome to start a competing coin and prove their superiority, so are governments. Despite their enormous head start, government fiat (paper) currencies have struggled to keep up with the blistering pace of investment and innovation available in Bitcoin (rising cryptocurrency market value is the same thing as declining fiat currency market value). A government could start its own variant of Bitcoin, and those attempts are beginning, but they are unlikely to find widespread public support. A coin that takes purchasing power or control away from end users to give to the government is not going to be popular, as each individual user can see it is in their own interests to avoid such a coin and instead buy Bitcoin or other cryptocurrencies which prioritise protecting end consumer purchasing power, privacy and global availability wherever possible.

In addition, even the largest government cannot hope to compete with a permissionless global community developing products and services for their favourite cryptocurrencies. There is simply too many, too motivated and too productive a market in private currencies. In the same way that a segregated "national Internet" by even the largest countries cannot hope to compete with the globally connected free-market Internet, government cryptocurrencies will not be able to compete with Bitcoin.

In this way government, no matter its access to or propensity for violence, has been placed between a rock and a hard place by cryptocurrency. Supporting it will undermine what control of the monetary system they still have, and yet outcompeting it is not a feasible alternative. Bans or other punitive measures on their own citizens are also not practical - besides being unpopular with the public, it simply drives economic innovation and industrial progress into more permissive rival countries. Furthermore, government officials and legislators themselves cannot long avoid the opportunity to be involved in cryptocurrency for the sake of their own finances, and are thus tempted into advocating for cryptocurrency to protect their own investments.

Government has met its match with cryptocurrency - a completely peaceful and endlessly motivated adversary that it cannot threaten, bribe, bomb, ignore, cover-up or switch off. This will fundamentally change world history, as without the ability to invisibly tax its populations by inflating the monetary supply, government will have to adjust its expenditures to a level that can be justified with direct taxation.

Ok so governments are in a losing battle against the rising tide of cryptocurrencies, now let's look at their partners-in-crime, the banks.

Episode 6 of 10: Banks

The initial response to cryptocurrency by the banking industry was to ignore it, or alternatively to slander it with a concerted campaign of what cryptocurrency communities call "FUD" - fear, uncertainty and doubt. All of the accusations about money-laundering, drug smuggling and more were ludicrous hypocrisy coming from an industry rife with criminal activity and exploitation. Grand predictions of cryptocurrencies downfall were proven incorrect time and time again. The slander campaign failed horribly, and cryptocurrency continued to grow and succeed in spite of bankers' vitriol.

At a certain point, it began to dawn on the banking system that if they didn't join the parade it would march past without them. They are now scrambling to get involved themselves, often while continuing to proclaim their lack of concern. Banks claim that cryptocurrency will have to operate on their terms, but that is self-evidently a lie. If cryptocurrency had to operate on banking terms, then the banks would simply shut it off - just as the government would. They cannot, and so they are wailing about their crumbling narrative while being swept aside by a tide of innovation they cannot negotiate with.

When Henry Ford invented the Model T, it would have been foolish of him to listen to or accomodate the demands of horse and carriage manufacturers. The top speed of a car is limited if it is tied to a horse. A new paradigm's potential cannot be hobbled by bothering to placate the incumbents it replaces. For the same reason, the cryptocurrency community is generally not that interested in negotiating with or accomodating banks, who are left to play catch up and make fruitless appeals to their cronies in government for help.

In the future, banks will not vanish but their primary business model of creating new money and enslaving the population through debts will no longer be feasible. Instead, they will likely become cryptocurrency wallet providers and continue to provide lending services - although with far better rates and customer service - due to growing competition from entirely automated cryptocurrency platforms.

To avoid the recreation of a new banking system, it is very important for new cryptocurrency adopters to understand how to hold their own cryptocurrency. The protection of a blockchain is that a "bank run" is impossible, as the blockchain always has 100% reserves for its promised supply, but that protection does not extend to anyone who then places their cryptocurrency in trust of a bank anyway. Holding your own cryptocurrency keys is called "self-custody" (as it is not given to a "custodial" service such as a bank). As global education spreads to safely hold and transact cryptocurrency with full custody, the banks become increasingly cut out as rent-seeking middlemen on people's use of money.

Alright that's enough about crypto adoption from the banks and governments, let's turn now to the beautiful but very messy and fraught process of cryptocurrency adoption.

Episode 7 of 10: Adoption, mania and scams

Remember in Episode 3 that Bitcoin itself is completely neutral - like any tool humanity has invented through engineering. It has no agenda, it simply exists, similar to email or the Internet. No one is in charge, it is a useful technology and Satoshi started the project without promising future riches in the misguided way that many cryptocurrency advocates do today. Bitcoin does truly have the superior monetary properties discussed in Episodes 1 and 2, and will gain increasing adoption for those reasons despite entrenched interests and personal distate by some individuals in society. Although it has these foundations, cryptocurrency faces constant accusations and doubt about being a scam or a Ponzi scheme - and not without reason.

"Is cryptocurrency a scam?" The actual answer is "No, but maybe." As we have discussed, the code for Bitcoin is completely open source, and anyone can make a copy and tweak it however they like. This has created a chaotic market of alternatives, which range from very legitimate competitors on the attributes of money, to self-avowed Ponzi schemes.

Consider that any form of government decreed money is essentially a very long-running Ponzi scheme. The last people to be holding Roman denarii at the fall of the Rome empire were essentially left holding the bag as the government inflated their purchasing power away to nothing. Same with those left with hyperinflating German Marks, Zimbabwean dollars or Venezuelan bolivars. With this in mind, the cryptocurrency community often mock government currencies (such as the US dollar or British pound) and minor cryptocurrencies alike for having poor monetary properties and thus being eventual scams that will not last the test of time.

It is up to each individual to assess the coins available (both fiat and crypto), and support those that have utility and a verifiably strong claim to having a chance at being a long-lasting form of money. The rest will fade away with time. It is safe to say that at least 99% of the 10 000+ cryptocurrencies available today will not survive the next 5, 10 or 20 years. Remember the cryptocurrency motto, "Verify, don't trust". Explore, but be skeptical, and remember the fundamental 6 properties of money from Episode 1 to guide you in your analysis. Find projects that have real people you can connect and trade with, avoid anything that promises a quick and easy path to riches, and do not invest in any coin unless you understand what is happening with it. These same ideas can be applied universally, but some specific coins are discussed in Episode 8 and Episode 9.

Cryptocurrency or Bitcoin itself makes no promises or guarantees to anyone, and involvement in any way is entirely voluntary. Its lack of regulation is a strong positive for the rapid economic development of the industry, but it means as an individual it is up to you to take responsibility for finding your own trust worthy information sources (you might choose this article series and podcast, or other cryptocurrency content creators for example). There is no ability to delegate responsibility to a government authority, as they have their own incentives to provide misinformation about cryptocurrency and largely cannot protect you from mistakes in cryptocurrency investing.

Cryptocurrency promotes a philosophy of free market experimentation, in fact very radically so, and as Uncle Ben told Spiderman "With great power, comes great responsibility". These scams have taken just about every form imaginable, due to malice, incompetence or both, and undoubtedly there will be many more.

It is easy for critics to point at this drama (or: experimentation) and paint it all with a broad brush of failure or illegitimacy. However, the solid layer of monetary properties in the largest cryptocurrencies that survive the brutal free market environment creates an undeniably rising floor of real economic activity. Cryptocurrency critics have all kinds of reasons they believe people won't adopt cryptocurrencies, but all of them have been proven false. The ongoing success of cryptocurrency is evidence enough of this, but let's quickly touch on a couple of the most common complaints:

Terrorism, scams, ransomware, sex trafficking, money laundering and other crime: The reality is that criminals use the same technology as everyone else. Terrorists and scammers are assisted greatly by the existence of US dollars, the Internet, running water and the telephone - because those things help everyone. Of course, no one would suggest we try and shut down the Internet, causing a huge loss to humanity generally, just to thwart a small portion of criminal activity. Bitcoin and cryptocurrencies are no different.

Volatility: As discussed with the futility of linking cryptocurrencies to physical assets, it is a feature (not a problem) of cryptocurrencies that their value is provided entirely by their monetary properties and the free-market demand to use them in peer-to-peer commerce. There is some truth to investor caution around volatility, but it isn't a deal-breaker. Once they understand the premise, investors actually love cryptocurrencies' volatility, because while crypto prices denominated against fiat currencies sometimes go down, on average the long lasting and solid projects go up much more often. Anyone buying cryptocurrency for the short term is either profiting from the volatility or will have spent it before the value has changed significantly, and anyone investing in cryptocurrency for the long term knows they will eventually be in profit as the value of fiat currencies continues to deplete. Particularly for individuals in hyperinflating economies such as Argentina or Turkey, downwards volatility is a guaranteed fact of life already with their fiat currency, so cryptocurrency is a huge plus if it also is sometimes volatile upwards. On top of this, the market has provided a variety of "stablecoins" to specifically address the issue of volatility. Finally, individual investors can allocate a small percentage that they are comfortable with initially, and increase their allocation as they grow comfortable or their existing holdings grow in value.

Note that investing in a cryptocurrency (and the accompanying volatility) is essentially a bet on the community that supports that coin. In the short term this can be very rocky, but in the long term it may be much more resilient and innovative than a central government which can collapse due to internal or external political factors.

Now that you understand Bitcoin, its philosophy, its opposition, and how it is becoming adopted, we can turn to the greatest controversy in cryptocurrency history and the reason for this entire website - the Bitcoin civil war which lead to Bitcoin Cash.

Episode 8 of 10: Bitcoin Cash

This is a very abbreviated history, a more complete & well-cited recitation can be found in Hijacking Bitcoin.

After its introduction in 2009, Bitcoin immediately became a smash hit. Despite the misinformation or doubts of its endless critics, the Bitcoin network exploded in popularity. More mining computers joined the network, transactions took off, and the project attracted interested computer enthusiasts, free market advocates and black or grey market vendors in droves.

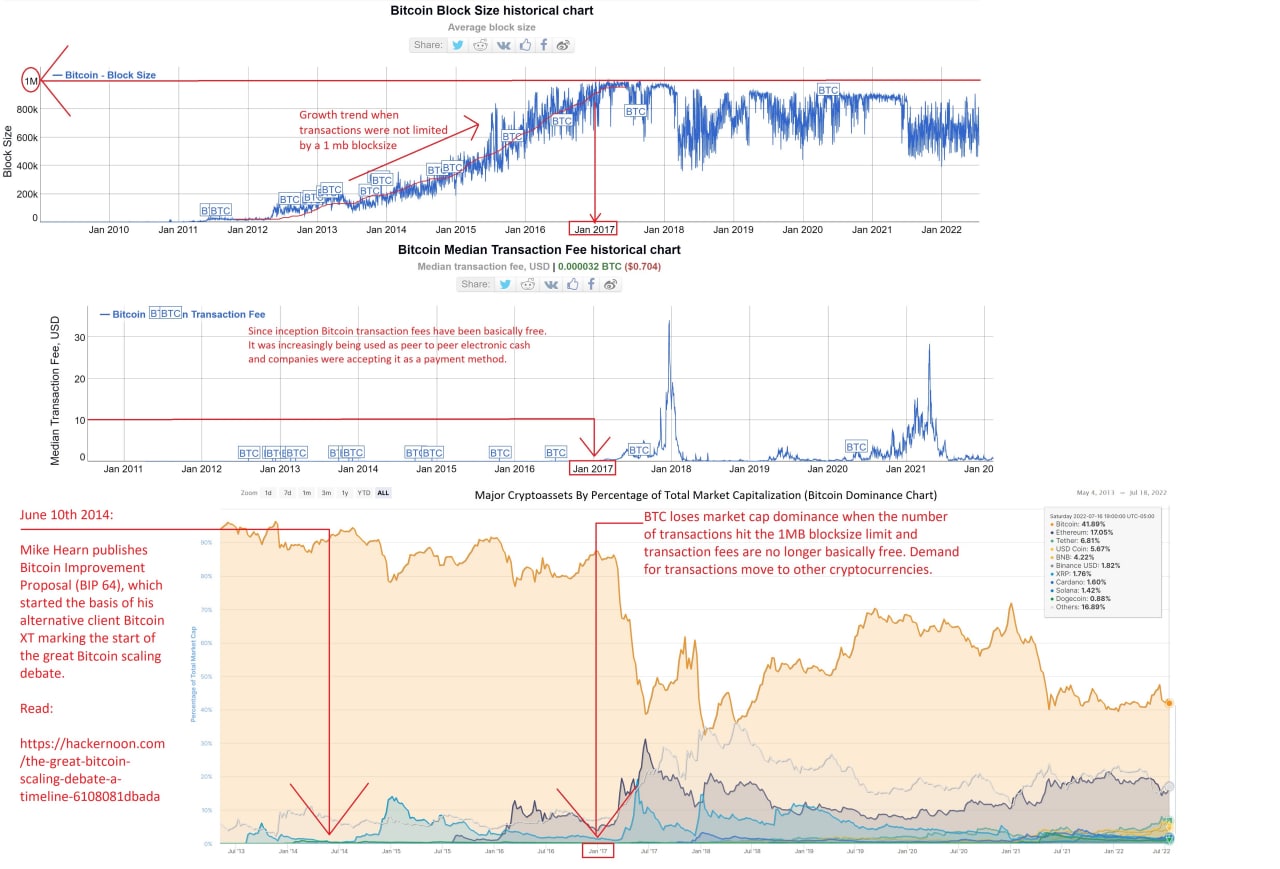

The network grew quickly. By 2012 Bitcoin was processing roughly 6 500 transactions per day. By 2014, that had grown to 65 000 transactions per day. And in 2016, over 200 000 transactions per day. In that same timeframe, the market price of Bitcoin had grown from $10 / coin, to closer to $700 / coin. Major retailers such as Microsoft and Steam were starting to accept Bitcoin for payments, and it seemed the fledgingly currency was breaking through to the mainstream.

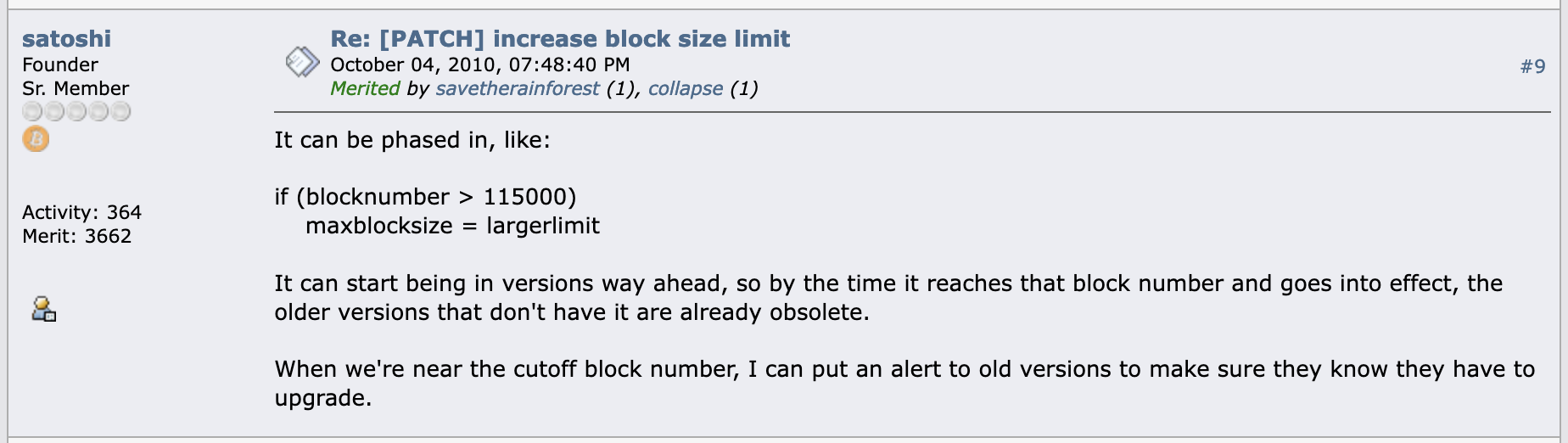

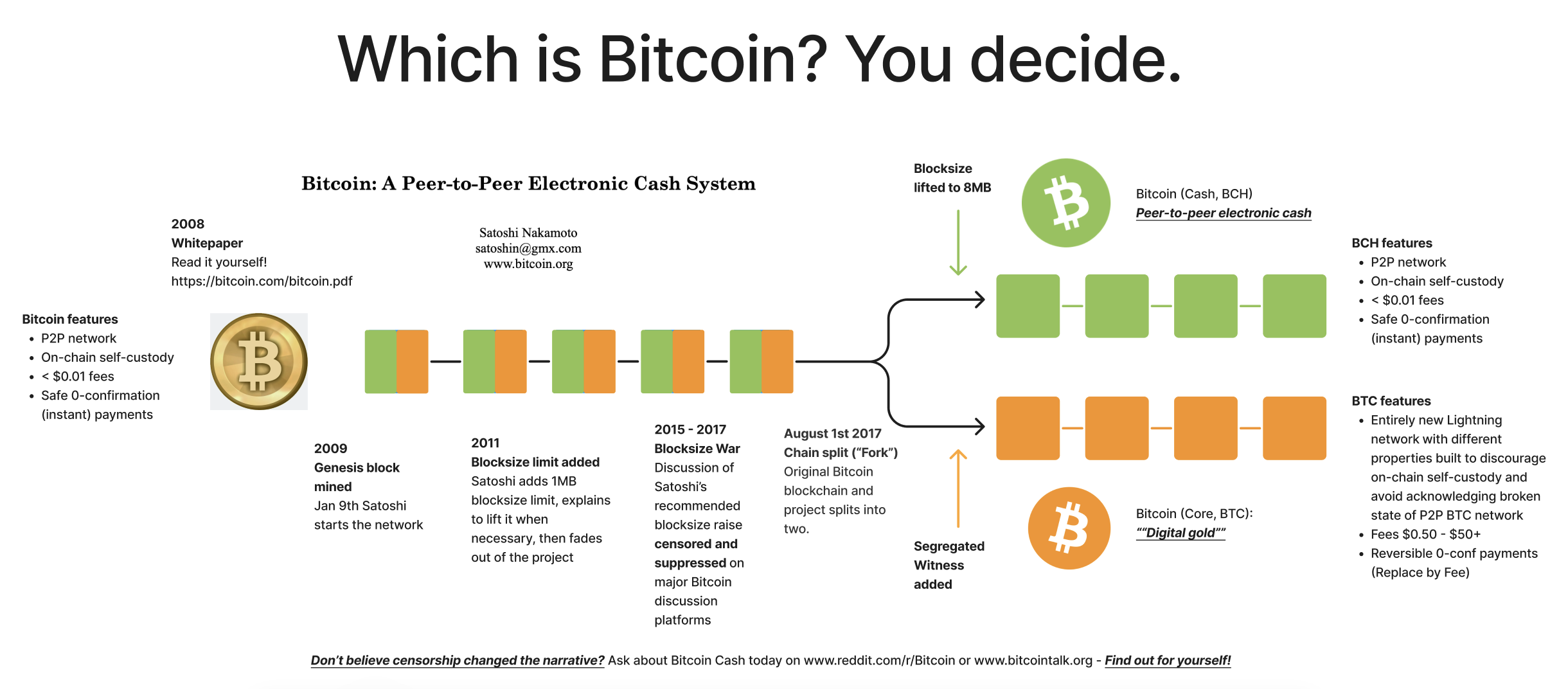

The community was overjoyed at Bitcoin's success. But there was a problem. Six years earlier, as a precautionary measure to protect the fledgling network, Bitcoin's creator Satoshi Nakamoto had limited the capacity of transactions to 1 megabyte per block (theoretically 7 transactions per second, around 3 in practice). He clearly stated this was a temporary measure, and provided instructions that the limit should be raised once real demand approached the throughput limit to maintain low fees. To Satoshi, it was a foregone conclusion.

Satoshi explains the plan to raise block size limit

However, this was the fly in the ointment in Bitcoin. As early as 2013, Satoshi's appointed successor to lead the project, a software developer called Gavin Andresen, began pushing for preparations to raise the blocksize limit. But in 2014, a new company emerged on the Bitcoin scene called Blockstream. This new company was invested in by AXA Group, one of the world's largest banking corporations. They declared that the 1 megabyte limit was essential to Bitcoin, and that its decreasing utility as a day-to-day currency was not a problem. Blockstream hired several prominent Bitcoin developers, who began to also advocate for this need to change track on Bitcoin's scaling plan. The blockchain could only handle 1MB of transactions, and as it was getting full, transaction fees started rising.

With no one authoritatively in charge, and no word from its long absent creator Satoshi, the Bitcoin community lapsed into what can only be described as a civil war. True to Bitcoin's peaceful philosophy, there was no guns or bullets involved, but instead a virtual war of ideas, debate, cyber attacks and manipulation. Although no one was physically injured, the debate reached a point of historical bitterness and division commensurate to any geopolitical civil conflict. Passions ran unbeliveably hot, in an energetic and unique community, largely comprised of individual's drawn to Bitcoin for ideological reasons.

On one side of the Bitcoin community was the "small blockers", who believed Blockstream's new plan for Bitcoin. They thought the 1MB limit should never be raised - believing high fees would pay for increased network security and that increased transaction volume would decrease the number of individuals able to run nodes on the network. On the other side was the "big blockers", who felt it prudent to follow Satoshi's original advice to raise the blocksize, thereby retaining low fees and expanding consumer adoption as a payments system. This period, which lasted roughly from 2015 - 2017, became known as "The Blocksize War".

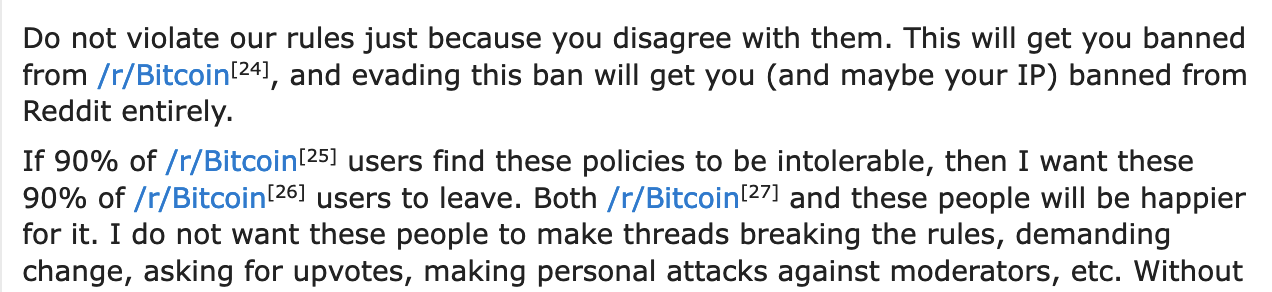

The central battleground for this conflict was the Bitcoin discussion section of the website Reddit, called /r/Bitcoin. As the Bitcoin community was still very small in size, a huge proportion of community discussion was happening there, and secondarily on the Bitcointalk forums. The head moderator of both forums goes by the username "Theymos", and has never been seen in public. He favoured Blockstream's "small blocker" plan, and he began banning any discussion of the "big block" side. Censorship of this kind was completely anathema to a community trying to build censorship resistant, authority free money - and the user base went ballistic. Community outcry reached such a point that Theymos took the unprecedented step of declaring that if 90% of users were unhappy, they should all leave instead of receiving an overwhelmingly demanded change in moderation policy or moderators.

Theymos exerts dictatorial control over Bitcoin discussion.

As the months ticked by, the rapidly growing community began to include a large segment of Bitcoiners that had never heard a fair discussion of both sides of the block size debate, further adding to the frustrations of the big-blockers. The big blockers had been an overwhelming majority of the "early Bitcoiners", but the exponential growing community size combined with censorship diminished their proportion dramatically. Several conferences involving prominent industry figures, developers, Bitcoin company representatives and miners were held to supposedly break this deadlock over "consensus", but with strange rules that no consensus could be achieved. Transparency of what occured at these meetings was very low to online observers, and negotiations over several compromises broke down as each side claimed the other was acting in bad faith. With internal community relationships at breaking point under a cloud of constant discussion supression, the small-block and Blockstream-employed developers seized control of the Bitcoin node software by kicking out Gavin Andresen and other "big block" favouring developers. With control of the code repository, they prepared to force through a controversial change to the Bitcoin protocol, called "Segregated Witness" - which they claimed would help retain Bitcoin's low fees - promising to accomodate a block size increase at a later date.

The market waits for no-one. Once the blocksize cap was hit, fees started rising and transactions, network effect and momentum predictably migrated to competitors. Big blockers trying to retain the original Bitcoin mission and success were under time pressure plus increasing censorship and community attacks, and the Bitcoin brand got stolen by the small blockers who have mismanaged it and continued to squander Bitcoin's market lead and potential ever since.

Marginalised from the discussion, tired of discussing compromises that seemed to be deliberate bad-faith delay tactics and anticipating a forthcoming betrayal, a team of "big blockers" enacted a desperate plan to preserve the Bitcoin project according to Satoshi's original whitepaper. The final resort of a dissenting minority in a cryptocurrency is called a "chain split" (NB: which is often incorrectly conflated with a "fork"), in which a single coin is fractured into two identical copies, which operate independently from that moment on. Holders of the original coin are granted an equal share in both chains, and can trade coins from one side against the other on exchanges as they would trade against any other crypto or fiat currency. Each community is then free to manage its side of the split (including their source code) as it believes prudent and compete directly on the free market. A chain split is irreversible, and the splintering of miners, nodes, businesses, developers and community members along ideological lines is a traumatic event for both sides - but particularly the dissenting minority. It is also highly risky, as mining attacks or lack of support can kill an ill-advised chain split entirely. It is only enacted under very dire circumstances, and since the invention of Bitcoin in 2008 the number of notable chain splits can be counted on one hand.

Those splits were chronologically (majority - minority):

2016: Ethereum (ETH) - Ethereum Classic (ETC)

2017: Bitcoin (BTC) - Bitcoin Cash (BCH)

2018: Bitcoin Cash (BCH) - Bitcoin Satoshi's Vision (BSV)

2020: Bitcoin Cash (BCH) - eCash (XEC)

3 of the 4 involve the Bitcoin Cash community, a unique and defining trait of its history - and great testament to the community's battle-tested resilience and passion.

As there was no precedent for the initial 2017 chain split between Bitcoin "small" and "big" blockers (the earlier ETH-ETC split happened under very different circumstances), there were many questions about the viability of the dissenting Bitcoin minority, with some predicting they would fail entirely to separate. The Bitcoin blockchain split in two on August 1st, 2017. It was a very rough landing, but it did stick. The big-block developers successfully coordinated a split despite pervasive doubts, enough Bitcoin miners supported the initiative, and the big-block chain survived without downtime. Despite advocating for a chance to compete fairly on exchanges and in the marketplace for the title of "Bitcoin", the big block side was mostly denied this initial equality by the risk-averse exchanges who didn't know how to handle such a novel event. With more pressing issues at hand than contesting the Bitcoin title and BTC ticker symbol, the new community coalesced on the name "Bitcoin Cash" and exchange ticker code BCH.

Visualisation of how Bitcoin split into BCH and BTC.

The big-block fears of betrayal immediately proved justified. As soon as Segregated Witness was implemented on the BTC side of the fork, discussion of promised block size increases was instantly quashed and the small block side rejoiced that they had vanquished their dissenting bretheren.

The Bitcoin Cash community became permanent exiles from the small block advocates. They lost the powerful and recognisable Bitcoin branding, but retained the original Bitcoin blockchain, their independence and the committment to Satoshi's original plan for a peer-to-peer currency used in direct daily transactions by the entire world. They also learnt to create multiple independent developer teams (so that developer or source code capture could not derail the project as it had with Blockstream) and to decentralise community discussion via more and more information channels (to circumvent any future censorship or disinformation attacks).

In the years following 2017, things changed significantly. The price of BTC rose immensely as the community retrofitted a new vision as "digital gold" which proved highly successful in the short term. However, fees also rose and adoption for payments went into reverse - Microsoft, Steam, Overstock and other companies stopped accepting Bitcoin as payment. With its anti-bank, pro-consumer origins crushed in the split with BCH, the BTC community instead sold their chain as a "store of value" solution to large banks and the authoritarian regime in El Salvador. Failing to scale as peer-to-peer cash opened a lot of extra room in the cryptocurrency markets though, and a host of other competitors led by Ethereum began rising to prominence.

Meanwhile, the price of Bitcoin Cash (BCH) cratered, as the community had to reorganise in the shadow of ongoing censorship, constant mockery and misinformation spread by the BTC side. But the BCH community battled on. Their mission was made even more difficult without the brand name, and with the constant need to educate newcomers on this critical history. Further drama ensued as new coins (Bitcoin SV and eCash) split off from BCH while the community established its own identity and governance. After 4 years (at the start of 2021), things stabilised and the BCH community finally appeared united and ready to begin seriously competing to be recognised as the best version of Bitcoin. Recognising this crucial turning point, I founded The Bitcoin Cash Podcast.

It remains true to this day that if BCH is able to turn the tide, catch up to and then overtake the BTC side of the split in terms of total users, market price and/or mining support (proof of work), the community will have a rightful claim to the original Bitcoin heritage and brand. Under such circumstances major exchanges and aggregators would be expected to return BCH the title of "Bitcoin" and the BTC community would have to rebrand (perhaps to "Bitcoin Core" or similar).

As you can no doubt guess, I was personally aligned to the big-block side, heavily involved in the community debate in the lead up to the split, and to this day advocate for BCH on my podcast. I believe the superior monetary properties and stronger community of BCH combined with Satoshi's genius original design will rise to prominence as more and more of the world begins transacting in cryptocurrency. BCH must prove itself like any other free-market money though, and I embrace the competition from other coins including BTC.

This ideological dispute over the "real" Bitcoin and it's "true" heritage motivates me individually, and it adds a lot to the motivation and narrative of BCH, but the coin can win simply on economics. Returning to the fundamental properties of money discussed in Episode 1, BCH has better portability, divisibility and fungibility (all due to lower fees) than BTC. BTC is not usable as a daily transactional currency, due to its high fees and poor transaction reliability, so BCH is an obvious alternative for anyone that actually wants to transact in the cryptocurrency economy. This difference in philosophy has many other ramifications, leading to a range of other issues with BTC. Money is simply a communication system that facilitates co-operation. Bitcoin Cash is the best money available to the world, and therefore its community will collaborate far more efficiently and effectively than all of its competitors. This allows its small but rapidly growing community to outcompete not only larger cryptocurrencies, but also all fiat currencies, given time for user education to continue and small edges to snowball.

Ever since the split in 2017, BCH & BTC have been diverging and are now substantially different. It's important to understand their shared history, but not to conflate them on other issues as a result. Sometimes they are the same, but increasingly they are not.

That's the story of the Blocksize War, the crucible of fire that uniquely began the life of Bitcoin under a rebranding as Bitcoin Cash. Most cryptocurrencies do not suffer such trauma though, so let's take a look at the other options in the next section on Ethereum, Dogecoin, Tether and all the rest.

Episode 9 of 10: Ethereum, Dogecoin, Tether and more

As early as 2011, Bitcoin had proven itself as an interesting idea in the market, and once that happened people started asking themselves "But what if I changed something? What if I made a coin with a larger supply, faster transactions, inbuilt taxation, more privacy or something entirely new?" Well the Bitcoin source code is freely available to anyone in the world, so people started experimenting. Today there are more than 10 000 cryptocurrencies available on the market place, each with their own twist on the original Bitcoin formula. You can even start your own cryptocurrency if you like, although most people will not as we will see in a moment. "This is great!" I can already hear you thinking, "I'll start my own Bitcoin and get rich!" Unfortunately, it's not quite that simple. Making a new cryptocurrency is easy because you can do that on your own, the hard part is what comes next - convincing other people to trade it with you. So let's take a second to talk about that.

The only thing money is useful for is buying stuff, and the only place to get that stuff is other people. If you think back to Episode 1, we talked about the six properties of money - scarcity, portability, durability, divisibility, fungibility, recognisability. History has shown that people gravitate to those six characteristics of money in deciding what to trade, but they are not fundamentally required for a system of money to exist. If your friend will allow you to loan money off them, it doesn't matter if the money exists purely inside both of your heads, it has value just because you both mutually agree on the transaction.

This is where the true power of cryptocurrency lies, with you. Now that you understand about cryptocurrency, it is up to you to make the free and voluntary choice of which cryptocurrencies you will accept as payment. It could be one, several, all of them or none at all, it's totally up to you. As billions of people around the world make the same decision for themselves, the most popular coins will rise to the top and become traded just as most people trade government fiat currency today.

There are more than 10 000 cryptocurrencies on the market today, we don't have time to address them all but broadly speaking they can be divided into three categories.

"Cash": Coins that are competing with Bitcoin (BTC) to become a globally used form of money. I like Bitcoin Cash (BCH), but other currencies have their own strategies for standing out for instance by adding additional privacy like Monero (XMR) or being funny like Dogecoin (DOGE).

"Stablecoins": Some coins seek to address the volatility property of cryptocurrencies by creating digital alternatives to the dollar that maintain a pegged 1:1 value. There are a variety of approaches to this, such as allowing tokens to be redeemed at a central bank account, or automatically generating tokens in proportion to the deposited value of other cryptocurrencies such as Ethereum or Bitcoin. The very significant risk of these coins is that they continue to devalue alongside the fiat currency they represent, plus the potential that the issuer begins to run a fractional reserve and cannot actually pay out the correct currency to cover the entire floating token supply. Examples of this include Tether (which is a scam) and USDC run by Coinbase. Other examples are created as "Algorithmic stablecoins" which come with their own risks and problems such as DAI, and the now-defunct, spectacularly imploded Terra (LUNA).

"Smart Contract Platforms": E.g. Ethereum (ETH), Cardano (ADA) or the SmartBCH sidechain of Bitcoin Cash. The first and largest smart contract blockchain is Ethereum, which was proposed in 2013 and later launched in 2015, as a variant on Bitcoin which extended the programattic capabilities of the blockchain itself. This idea of adding extra capability to money has led to the rise of "DeFi" or "Decentralised Finance", which is the idea that blockchain-secured assets can be used in new and innovative ways beyond the simple act of transferring units of money.

However Ethereum has suffered similar problems to Bitcoin (BTC) (albeit for technical reasons, rather than political ones), and increasing popularity has created enormous network fees. Because of this, we have seen an explosion of similar competitors that are interoperable with the same new financial products and code. This is called being "EVM-compatible". "EVM" stands for the "Ethereum Virtual Machine", the programming standard which Ethereum pioneered, so other coins can copy this standard in order to be compatible with many of the same applications. In the same way as coins compete with Bitcoin to be money, coins compete with Ethereum to offer the best array of open financial products - vying to stand out with different technical properties, community initiatives or other features. As with Bitcoin, no competitor has yet overtaken Ethereum but there is very fierce competition.

I highly recommend everyone to take a very, very small amount of money and experiment with the different coins available today. Every coin has its own community, attitude, uses, strengths and weaknesses. It's a free market, and every coin is competing for your interest as a consumer and community member and ultimately it is up to you to decide which ones provide the utility you are looking for. Almost all cryptocurrency holders have a distribution of coins, so it's up to you how strongly to align yourself with any given community and you can switch at any time. In cryptocurrency, the phrase "vote with your dollars" is literally true.

Episode 10 of 10: The future

Where cryptocurrency is going next is anyone's guess. One obvious prediction is that sooner or later, every single person in the world will own and trade in cryptocurrency - just as it won't be long before everyone in the world has access to the Internet. Critics will find themselves increasingly obsolete and eventually need to join up because anyone they want to trade with will no longer bother with fiat currencies which have become worthless in any case - likely inflated away with massive currency printing to try and pay off unpayable national debts.

How we're going to get from here to there is something being discovered day by day, and comes with a huge array of problems, debates, scams, education, entertainment and surprises along the way. There is currently an enormous market in cryptocurrency education and news services such as The Bitcoin Cash Podcast, and that is only set to continue. Current and future crypto influencers are going to blow up to household names. Corporations and institutions will launch cryptocurrency initiatives, perhaps their own coins for brand supporters.

But that's simply the beginning. As the world begins to understand and adopt the ideas of voluntary co-ordination at scale and as governments lose primacy over the printing of money, we will see much larger changes in society. The lowering of economic barriers between individuals in separate countries, as well as the access to financial services to billions of people in the poorest parts of the world who are priced out or not served by traditional banking services will have a titanic impact on global prosperity. The ability to safely accrue personal capital without inflationary debasement will change the lives of billions more, even those with access to existing banking infrastructure.

We have already seen cryptocurrency start to make impact on culture with the rise of NFTs. These "Non Fungible Tokens" are essentially a variation of cryptocurrency where each coin is individually stamped - allowing them to be collected or traded like trading cards or stamps. In my personal opinion, a handful of these projects will become insanely valuable status flexes while the vast majority that have value today will become irrelevant - similar to early ".com" domain names - some of which lasted until today as amazing online real estate and most didn't.

We have also seen new forms of direct charity. Because cryptocurrency can be sent to anyone, anywhere through as little as a picture and with the ability to publically verify that funds were spent appropriately on the blockchain it is conceivable we will see huge increases in charitable action. If you would like to investigate this more, I recommend eatBCH which funds meals for children in Venezuela and South Sudan using Bitcoin Cash.

Looking even further into the future and things get even more significant. As cryptocurrency becomes an accepted form of money throughout the world, governments will completely lose control of their national economy. This is not something to be scared of. Once upon a time people believed that the church and state needed to be one institution and it was impossible to run a society without them united. Today we know that is false, and looking back it seems ludicrous that people believed otherwise. The same is going to happen with the separation of state and money, and though some people might be tentative, on average things will work out fine. It will change up some things though. Government's will no longer be able to recklessly print money to fund expenses, instead any funding most come directly from citizens. Direct taxation has a limit, as excessive direct income taxation guarantees revolution (excessive indirect inflation taxation guarantees hyperinflation). This will lead to harder choices by the government about what the people of their country will prefer funding and almost certainly one of the first expenses to be slashed will be the enormous waste on expansionary military policies. This will bring about a massive decrease in global conflict (as some countries de-escalate military spending, other countries are free to do so as well in a positive feedback loop). This is a key motivation in the humanitarian aspect of cryptocurrencies. Keep in mind that any government is free to start their own cryptocurrency (which they are doing, see CBDC Tracker) and compete with the free market to offer the best form of money - but for the reasons explained previously they will only struggle harder and harder than they already are.

As the world reduces its reliance on and defunds centralised governments, new forms of human co-operation will arise. There has already been exploration of the idea of "DAOs" (Distributed Autonomous Organisations), which is kind of like a company or charity if it had no hierarchy or CEO. Such concepts are in their very early stages, and have encountered their own trials and tribulations along the way, but with time and experimentation it is almost certain we will discover a slew of effective new ways to collaborate among individuals, across borders and with new sets of binding incentives that will augment or obsolete familiar society structures.

What else will come out of this engine of permissionless innovation and free-flowing value transfer is impossible to forecast, but given a few billion people working on it it's a certainty that we will see cool new advancements in money, society and culture.

Conclusion

I personally believe that as more and more people understand and adopt cryptocurrencies as the most efficient payment system and incorruptible wealth storage, Bitcoin Cash will become the most used currency in the world - replacing the USD and most other fiat and cryptocurrencies. This is due to the proven resilience of its community discussed in Episode 8 and adherence to the properties of money discussed in Episode 1. For more detail, see Why Bitcoin Cash instead of another cryptocurrency?.

But that is merely my opinion. Who knows what the future holds, the only thing guaranteed in cryptocurrency is that it will change fast and always be surprising.

Either way, with the foundation acquired in this series you will be on much stronger footing in your own research and involvement with cryptocurrency. As I mentioned previously, go and experiment! Try out different cryptocurrency communities, ask questions, and stick to the cryptocurrency motto "Verify, don't trust". Be financially responsible by only using tiny amounts of money while you are unfamiliar with new technologies and if you need help there are plenty of passionate cryptocurrency forums online or in-person meetup groups to assist you.

If you'd like to join me on this journey, to build a more free and open world with Bitcoin Cash as the global reserve currency, you can subscribe to The Bitcoin Cash Podcast. I follow the evolving history of this technology with a podcast episode about once every fortnight, joined by a variety of guests discussing Bitcoin Cash and cryptocurrency in general. The show is distributed on Odysee, Youtube, Apple Podcasts, Google Podcasts, Spotify, Telegram and more. Links to all platforms can be found at the bottom of the page on www.bitcoincashpodcast.com. At the website there is also a lot of links to Recommended Resources, an FAQ section and more.

I hope this series has been informative, interesting and encouraging. Thank you for reading, and my eternal gratitude to Satoshi Nakamoto for the miraculous gift of cryptocurrency.

If you want to get involved immediately, you can take a look at these quick onboarding videos to download a wallet and join the cryptocurrency economy: